American household debt reached new heights in 2025 and continues to rise.

According to the Federal Reserve, U.S. debt climbed to $18.59 trillion last year, driven by rising mortgage balances and more than $1.2 trillion in credit card debt. Higher interest rates mean balances take longer to pay down, and everyday expenses are increasingly financed with credit.

Inflation—especially food, housing, and essential costs—continues to be the top financial concern for Americans. Nearly 60% say higher prices have made their finances worse over the past year. For many households, debt is starting to feel like a permanent, inescapable problem.

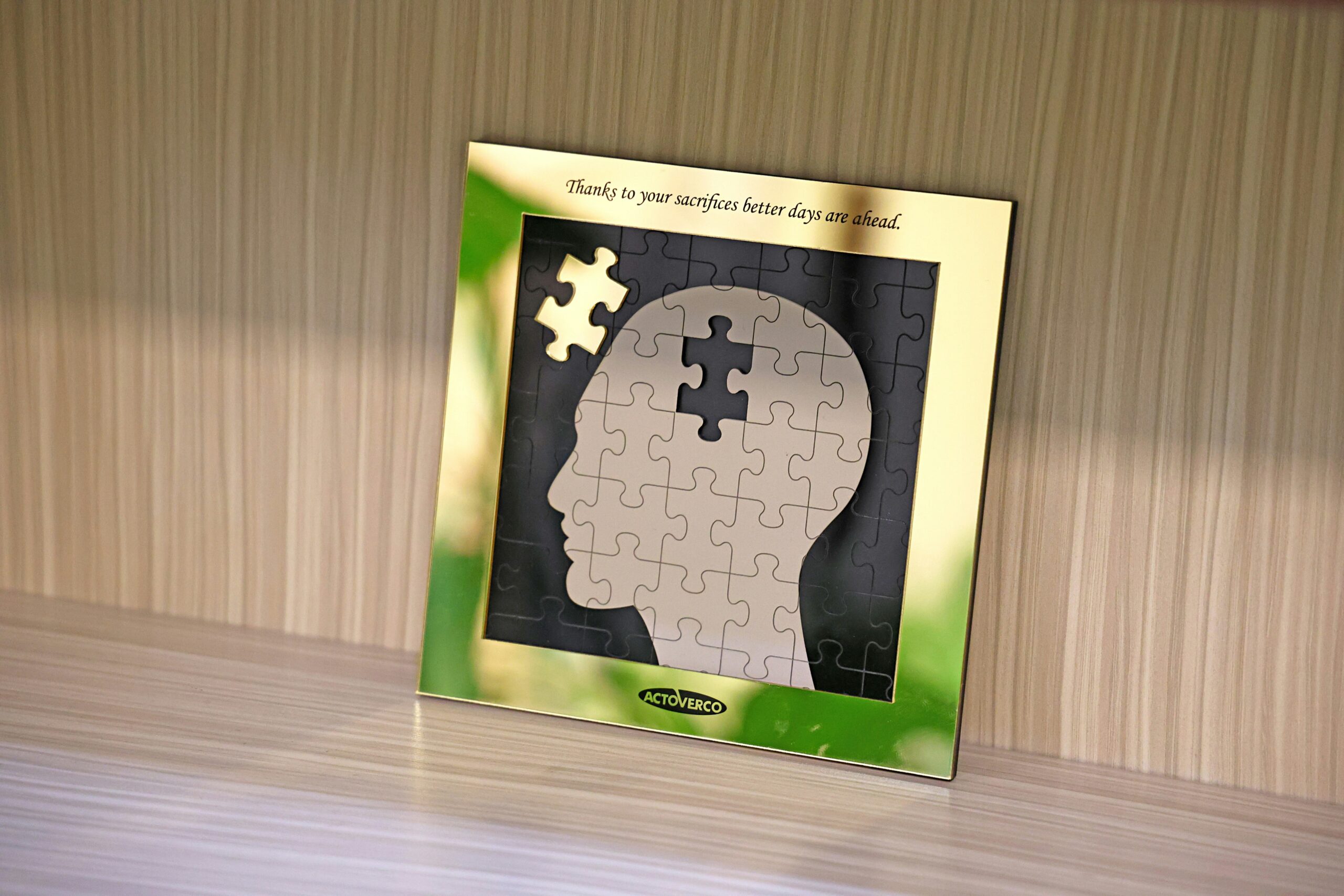

When people believe there’s no way out, they delay decisions, avoid opening mail, and disengage from the problem entirely.

But just as debt continues to rise, so do technology solutions that help consumers face their financial struggles and find resolution. Solo is at the forefront of this pioneering effort, and with AI-powered debt resolution tools, has helped consumers face more than $2.4 billion of debt.

Solo is disrupting the debt resolution space

Traditional debt resolution paths—lengthy phone negotiations, mailed paperwork, or months of back-and-forth—often feel outdated in a digital-first world.

Solo is stepping up to the challenge and creating AI-powered tools to disrupt the archaic debt settlement industry. One such tool is SoloSettle—an online, self-directed settlement negotiation tool that helps consumers negotiate and resolve debts more efficiently. SoloSettle is radically different from traditional settlement methods in 3 key ways:

- Speed: People can settle debt on SoloSettle’s platform instantaneously. Most debts on the platform are settled within 6 days.

- Affordability: Most debt settlement companies charge exorbitant fees. SoloSettle guarantees settlement and offers a variable commission fee structure to ensure maximum savings for consumers.

- Legal help included (if needed): Users who are sued for debt can access SoloSuit in conjunction with SoloSettle to draft and file a written Answer with the court, send it to the opposing attorney, and avoid a default judgment. Filing an Answer gives consumers greater leverage to settle, and it saves creditors time and resources that they would otherwise spend on court costs and attorney fees.

Legal solutions are baked into Solo’s process

While many consumers pursue informal resolution, debt increasingly enters the court system. According to a Pew Charitable Trusts report, debt collection lawsuits increased by 120% in some states in recent years. Solo offers a legal solution called SoloSuit for consumers who face legal debt issues.

Think of SoloSuit as the “first responder” for debt lawsuits. Instead of facing a wall of complex legal jargon, users complete a simple online quiz. The platform’s logic engine, specifically tailored to debt collection laws in all 50 states, converts these answers into a legally valid Answer document.

Unlike other legal sites that provide a generic PDF, Solo handles the “last mile” logistics. They calculate filing fees, cut the checks to the court, and mail the documents, ensuring the defense is officially recognized before the deadline.

Since less than 10% of people who sued for debt can find a lawyer, SoloSuit is a game-changer for consumers seeking full resolution.

Resolution offers Americans financial stability

As debt disputes scale faster and reach further into the legal system, the need for accessible resolution options is more urgent than ever.

Resolution-focused solutions are becoming a critical part of America’s financial ecosystem. Rather than delaying the inevitable, more Americans are seeking faster, more transparent ways to close the loop on debt. Solo offers a digital path to full resolution, helping consumers find the financial stability that is increasingly rare in today’s economy.

As more Americans prioritize paying off their debts, Solo could be the solution to disrupting the country’s financial ecosystem, lowering interest rates, increasing creditor trust, and improving the overall economy.

Written in partnership with Tom White