Image Credit: BOSS Money

Sending money across borders used to feel like a separate financial errand. It usually required visiting a storefront, filling out information, checking fees at the counter, and hoping the recipient could get the funds without a delay. For many families, that process was simply part of supporting relatives abroad, but it was rarely convenient.

That experience is beginning to look much more like the rest of consumer finance. People already manage bank accounts and manage their finances from their phones, so it was only a matter of time before consumers expected the same for international money transfers. Users want to know the fee before they send, see the exchange rate clearly, choose how the money will be delivered, and track the transfer without calling customer service or waiting in line.

The transition matters because cross-border payments are not casual things for most users. A transfer might help with groceries, school costs, rent, medical bills, or other household expenses for relatives in a different country. When people send funds for essential needs, speed and clear messaging are usually key priorities.

That appears to be influencing how international money transfer companies compete. Price still matters, especially for people sending money often or in smaller amounts, but the cheapest option is not always the one people trust with an urgent transfer. A reliable app has to make users feel confident before they press send, then keep them informed until the money arrives.

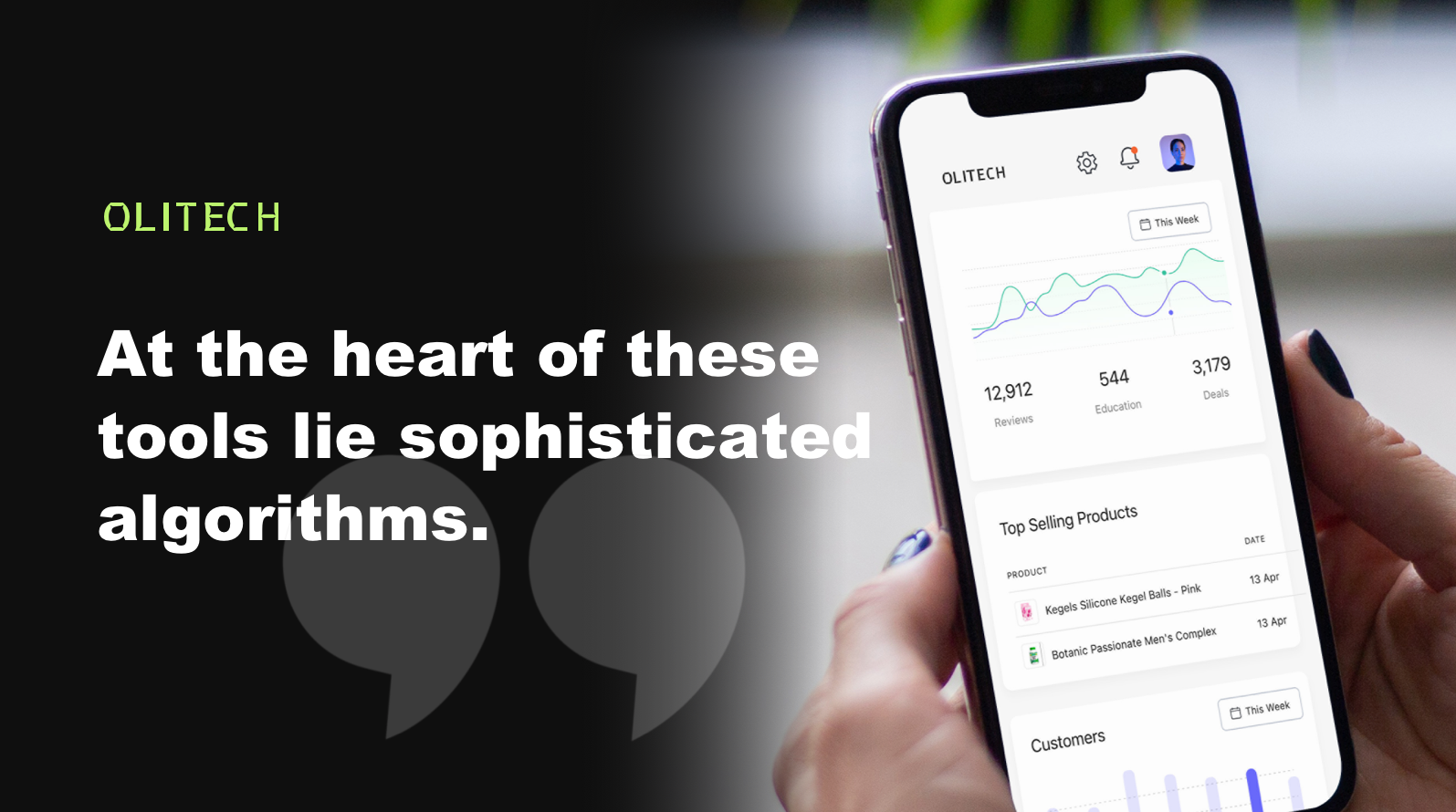

BOSS Money, a Newark, New Jersey-based international money transfer app, is one company operating in that middle ground between affordability and trust. According to the company, the platform allows users to send money to more than 50 countries through options that include cash pickup, bank deposits, mobile wallet transfers, home delivery, and direct-to-debit transfers. It also supports local currencies such as the Mexican peso, Bangladeshi taka, Ghanaian cedi, and Nigerian naira, giving users a way to send funds in forms that recipients can actually use.

“BOSS Money was built for people who need a simple, fast, and affordable way to send money across borders to friends and family,” said BOSS Money’s Bill Pereira. “Whether you’re sending $10 or $2,000, we make sure your money arrives quickly and securely.”

That range of transfer sizes is important. International remittances are often discussed in large economic terms, but the individual transactions can be modest and frequent. A user may send a small amount one week and a larger amount the next, depending on family needs, exchange rates, or timing. For those customers, a good transfer app has to be easy enough for routine use but secure enough for moments when the stakes feel higher.

Greater transparency is one of the trends that has accompanied this evolution. BOSS Money includes live fee and exchange-rate previews, along with a built-in calculator showing how much the recipient will receive before the sender confirms the transfer. That kind of visibility may help address one of the long-standing frustrations associated with remittances, where fees, exchange rates, and final amounts have not always been easy to compare.

BOSS Money also includes security features such as Face ID and passcode security, fraud alerts, encrypted transactions, and real-time tracking. These details may sound routine in a banking app, but they carry particular weight in cross-border payments because the sender and recipient are often separated by time zones, banking systems, and local pickup networks. A delay or uncertainty can quickly create anxiety on both sides of the transaction.

The broader lesson is that international money transfer is becoming less like a specialty service and more like a normal part of mobile banking life. Many money transfer apps aim to make transfers faster while providing features that can help reduce uncertainty throughout the process.

That may be the real change. Sending money abroad will always involve more complexity than sending money across town, because currencies, regulations, delivery networks, and local payment habits all matter. For many users, the experience may feel simpler and easier to navigate than in the past. For families that rely on these transfers, those improvements in usability can be a meaningful part of the overall experience.

The information provided in this article is for general informational and educational purposes only. It is not intended as financial advice. Readers should not rely solely on the content of this article and are encouraged to seek professional advice tailored to their specific circumstances. We disclaim any liability for any loss or damage arising directly or indirectly from the use of, or reliance on, the information presented.

Written in partnership with Tom White